2024-01-29

Stiritz became CEO of Ralston Purina in 1981 at the age of 47. Ralston Purina is a company that sells agricultural feed products for animals. Stiritz had already been with the company for 17 years, joining in 1964 and becoming the general manager of a division in 1971, where he increased operating profits fiftyfold through a relentless program of new product introductions and line extensions. Dean, the previous CEO, used much of the cash flow in engaging in a diversification program that left the company with a melange of operating divisions. When he announced his retirement, Bill Stiritz wrote him a letter outlining how he would turn the company around after the stock price had not reached new highs in a decade. He got the job.

He started aggressively restructuring the company around these businesses, which he believed offered an attractive combination of high margins and low capital requirements. He sold all the businesses that did not meet his criteria for profitability and returns. He sold the Jack in the Box chain of fast-food restaurants, the mushroom farms, and the St. Louis Blues hockey franchise, along with other non-core businesses. He used the proceeds from the sales and put them into higher-returning areas of the business. With a natural facility for numbers and a skeptical, almost prickly temperament, in the 1980s, he initiated buybacks while peers did not. Additionally, he made two acquisitions, both representing 30% of Ralston's enterprise value, financed with debt: Continental Baking, maker of Twinkies, and Energizer Battery for $1.5 billion. He was willing to pay an admittedly full price for an asset he felt had a uniquely attractive combination of a growing duopoly market and undermanaged operations. He further acquired underperforming companies.

Ralston was really diversified when Stiritz noticed that some business units did not receive the attention they deserved; he would spin them off. He further executed buybacks and spinoffs after selling the company for $10.4 billion to Nestle, achieving a 14x cash flow.

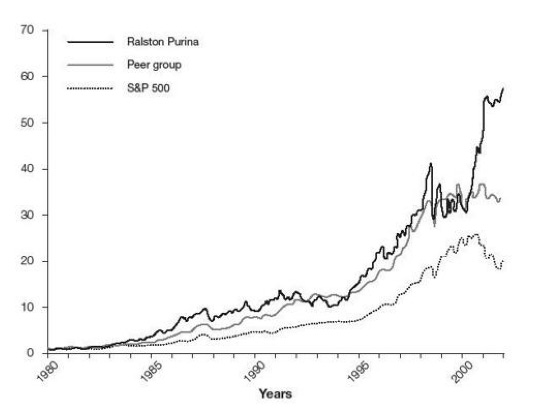

20% vs 17,7% peers and 14,7 S&P 500

"Effective capital allocation requires a certain temperament. To be successful, you have to think like an investor – dispassionately and probabilistically, with a certain coolness. Stiritz had that mindset." - Michael Mauboussin

He was an active acquirer who was also comfortable selling or spinning off businesses that he felt were mature or underappreciated by Wall Street, often using leverage to finance these, similar to KKR with a high debt-to-cash flow ratio. The primary flows were asset sales, cash flow, and debt.

He made concentrated buybacks at low P/E multiples. "The hurdle we always used for investment decisions was the share repurchase return. If an acquisition, with some certainty, could beat that return, it was worth doing."

He liked companies that had been undermanaged, preferred direct contact with sellers, and avoided auctions. For example, he brought Continental from ITT with a letter to the chairman.

He focused on a handful of key variables: market growth, competition, potential operating improvements, and, always, cash generation. "I really only cared about the key assumptions going into the model. First, I wanted to know about the underlying trends in the market: its growth and competitive dynamics."

"When the opportunity to buy Energizer came up, a small group of us met at 1:00 PM and got the seller’s books. We performed a back-of-the-envelope LBO model, met again at 4:00 PM, and decided to bid $1.4 billion. Simple as that. We knew what we needed to focus on. No massive studies and no bankers." It involved a single sheet of paper and an intense focus on key assumptions, not a forty-page set of projections.

"Stiritz ran Ralston somewhat akin to an LBO. He was one of the first to see the benefit to shareholders of higher leverage as long as cash flows were strong and predictable. He simply got rid of businesses that were cash drains (no matter their provenance) and invested more deeply in existing strong businesses through massive share purchases interspersed with the occasional acquisition that met our return targets." - Mulcahy

He questioned the status quo, including Wall Street accounting shenanigans. The CEO must be independent-thinking; most CEOs come from legal, marketing, sales, and are always dependent on their bankers or CFOs.

He was skeptical of advisors and investment bankers; he described them as "parasitic." He negotiated in meetings by himself. "Some people are innovators and some people borrow ideas from others. Stiritz is both."

This still is from my Outsider series

Thanks,

Finn